News that matters globallyReporting on public life and major developments across the U.S., the UK, and beyond.

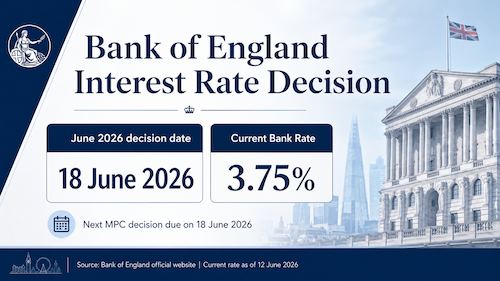

The next Bank of England interest rate decision is due on Thursday 18 June 2026. Bank Rate is currently 3.75%, and mortgage, savings and borrowing customers should check the official MPC statement before acting.

The next Bank of England interest rate decision is due on Thursday 18 June 2026. Bank Rate is currently 3.75%, so mortgage, savings and borrowing customers should wait for the Monetary Policy Committee statement before assuming any change to their own rates.

The Bank of England lists the June Monetary Policy Committee announcement and minutes for Thursday 18 June 2026. The Bank says its Monetary Policy summaries and minutes are published at 12 noon on a Thursday eight times a year.

The June decision has not yet been published. On decision day, the official page should show whether Bank Rate has been held, cut or raised, along with the vote split and minutes.

The current official Bank Rate is 3.75%.

The latest published decision was the April 2026 MPC meeting. The committee voted by 8 to 1 to maintain Bank Rate at 3.75%, with one member preferring a 0.25 percentage point increase to 4%.

Bank Rate was last changed on 18 December 2025, when the official Bank Rate history shows it moved to 3.75%.

The first figure to check is the new Bank Rate. Next, check the vote split: a narrow or divided vote can be useful context, even when the rate itself is unchanged.

Readers should also read the opening paragraphs of the Monetary Policy Summary. That is where the Bank explains why the MPC judged that rate level appropriate, and what the committee says it will watch next.

For June, there is no Monetary Policy Report listed on the MPC dates calendar. The next date with a Monetary Policy Report is Thursday 30 July 2026.

Bank Rate is not the rate on a mortgage, loan or savings account. The Bank of England describes it as the rate it pays to commercial banks, building societies and financial institutions that hold money with it, and says changes in Bank Rate influence — but do not exactly determine — the rates banks offer customers.

For mortgage holders, the product type matters. MoneyHelper says fixed-rate mortgage payments stay the same during the fixed period, while variable-rate mortgages can move up or down, usually in line with Bank Rate. Tracker mortgages normally follow a linked rate, often Bank Rate plus a set margin.

Savings rates do not always move automatically either. MoneyHelper says banks do not always increase savings rates when Bank Rate rises, so savers should check the rate they are actually being paid and compare it with available accounts.

The safest source on the day is the Bank of England’s own Monetary Policy Summary and minutes page for June 2026. The Bank’s main monetary policy page also lists the current Bank Rate and the next due date.

After the decision is published, check your lender or savings provider for any account-specific change. A Bank Rate decision can affect pricing across the market, but the timing and size of any change depends on the product and provider.

This article should be refreshed after the Bank publishes the June decision, with the new Bank Rate, vote split and any key wording from the MPC statement.